INSIGHTS

Italy's natural private market

which does not yet have its infrastructure

Succession, governance and patient capital to protect and grow strategic SMEs.

Askéon Capital | 15 Dec 2025

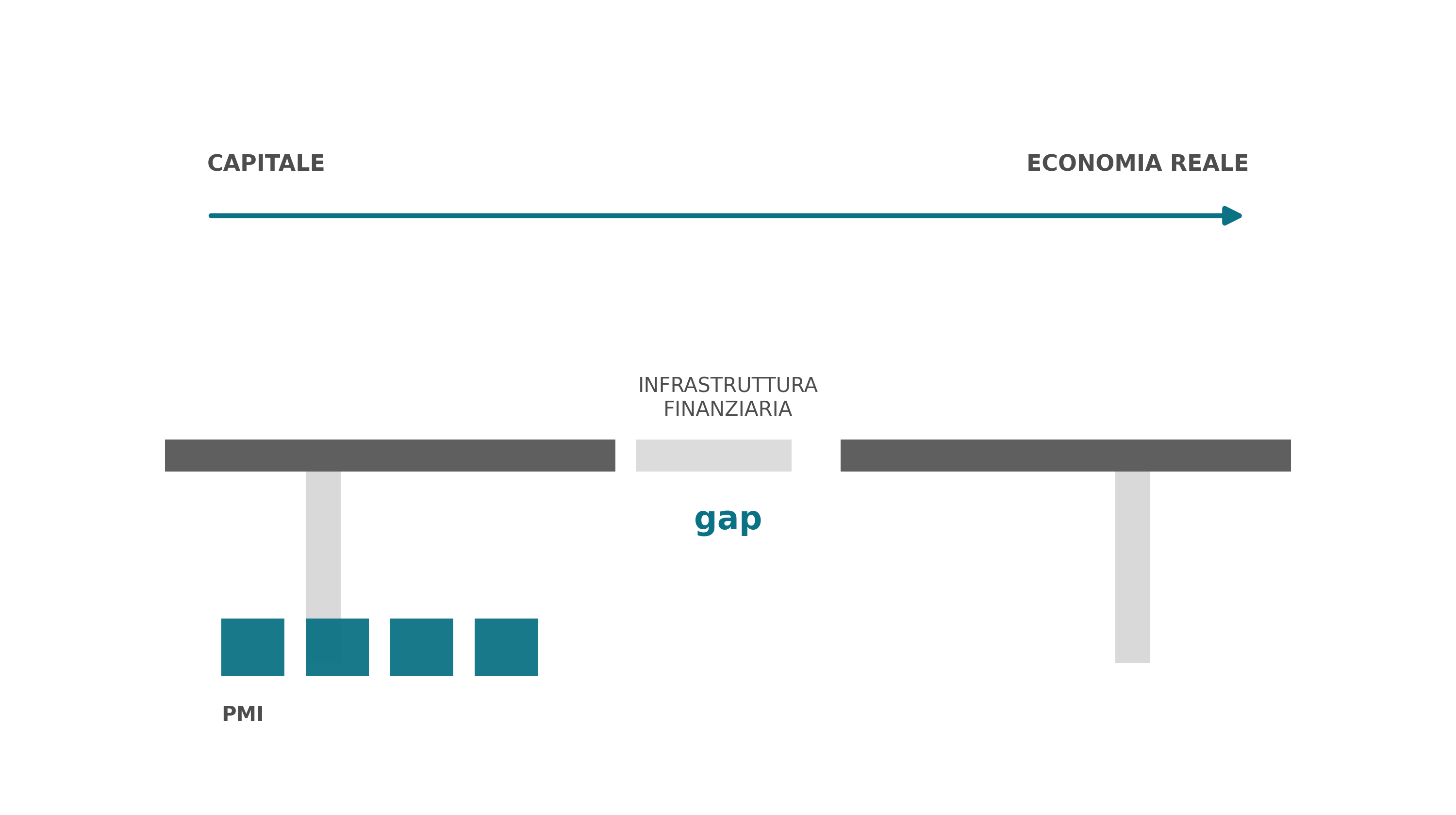

Figure — The infrastructure “gap” that prevents capital from efficiently re-entering the real economy.

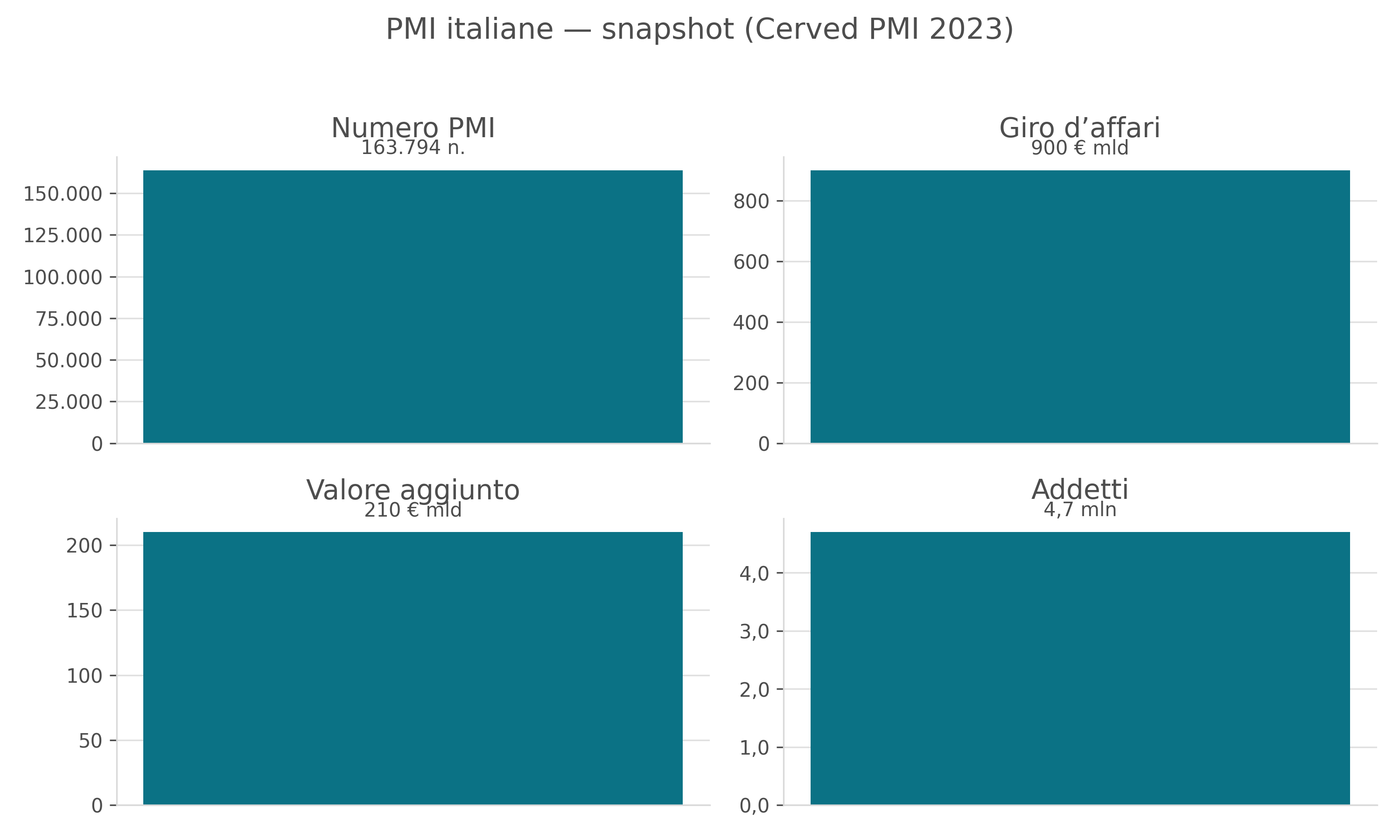

Italy is not just a country of SMEs. It is, in fact, a natural private market that has not yet built its own coherent financial infrastructure. Micro and small businesses make up approximately 99% of companies, generate over 60% of added value and employ approximately 75% of workers. Within this fabric, family businesses are the norm: between 85% and 90% of companies are family-controlled.

FIGURE 1 | SMEs: economic and employment scale

Source: Cerved PMI 2023.

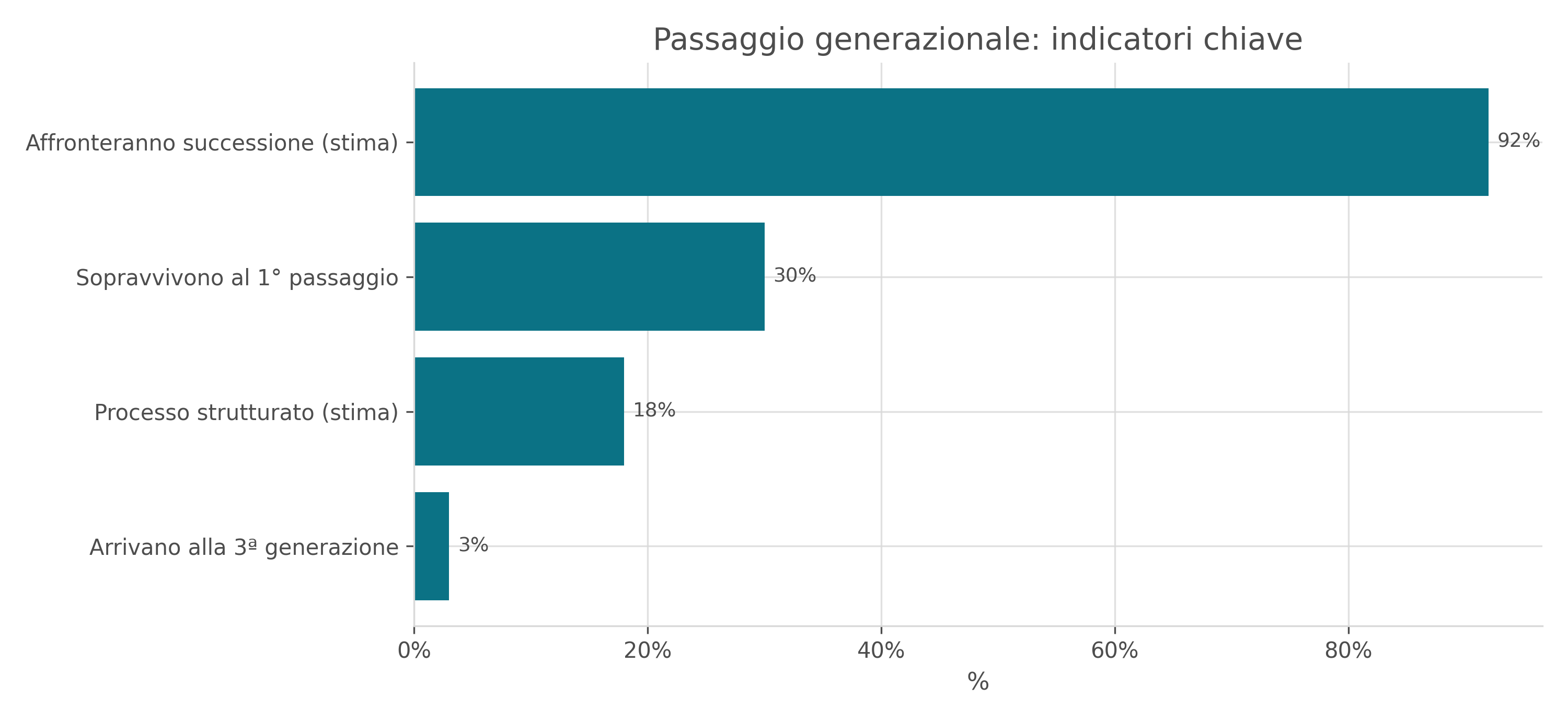

Regarding the generational transition, the numbers are merciless: only 30% of family businesses survive the first transition, and just 3% reach the third generation. A recent estimate indicates that 92% of Italian family SMEs will face a succession in the next few years and that only 18% have a structured process. In a country where almost all businesses are SMEs and almost all SMEs are family-run, every succession is a systemic event. In the next five years we are likely talking about hundreds...

FIGURE 2 | Generational change: key indicators

Source: values reported in the text (estimate/literature).

In many sectors, Italy has built global niches with high added value: foundries and precision mechanics, advanced manufacturing for automotive and aerospace, components, manufacturing for design and fashion, quality agri-food. They are companies with a few tens of millions in turnover but a density of know-how that is difficult to replicate, true "pocket multinationals". They are not very interesting for global conglomerates - too specific, too based on tacit knowledge - and at the same time too small and fragmented for big global capital, which thinks in tickets worth hundreds of millions. The result is that the country's most valuable asset is structurally undercapitalized and undergoverned, despite generating healthy cash flows and high potential margins.

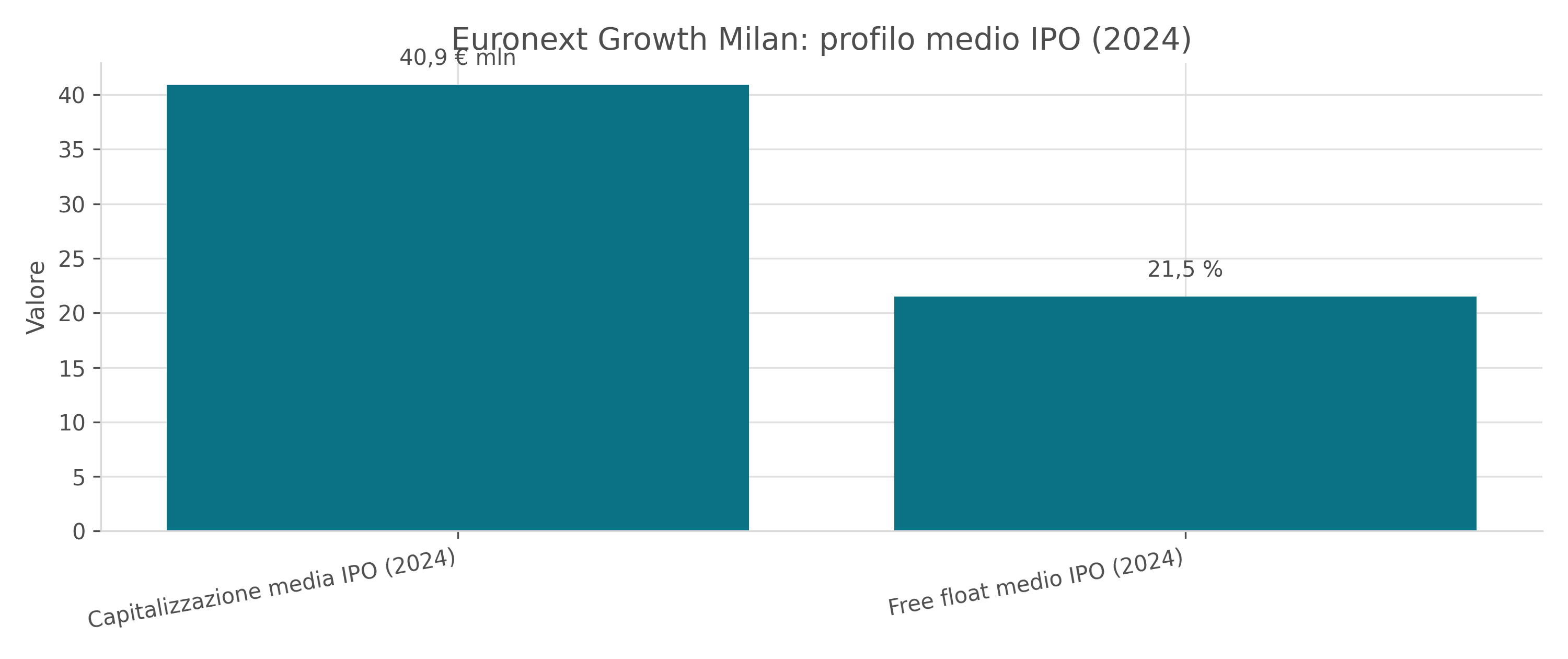

The reflex response is: "let's go to the stock market". But for the majority of Italian SMEs the stock market is a mirage, if not a delusion. At the end of 2024 the entire list was worth around 836 billion euros, just over a fifth of Nvidia and a third of Amazon: a sign of insufficient depth in the stock market. On the Euronext Growth segment, dedicated to SMEs, the average capitalization in IPO is around 40 million, with free floats in the order of 20%: for many companies the actually negotiable capital is reduced to 10-15 million euros. The result is subtle trades, prices that are often disconnected from fundamentals, and difficulties in making serious capital increases. The growth in delistings indicates that it is not the individual issuer that is not working, it is the architecture. Telling an SME that wants to grow and aggregate "go to the stock market and solve it" is, in most cases, the wrong answer to the right question.

FIGURE 3 | Euronext Growth: typical IPO size and free float

Source: IRTOP (average IPO profile 2024).

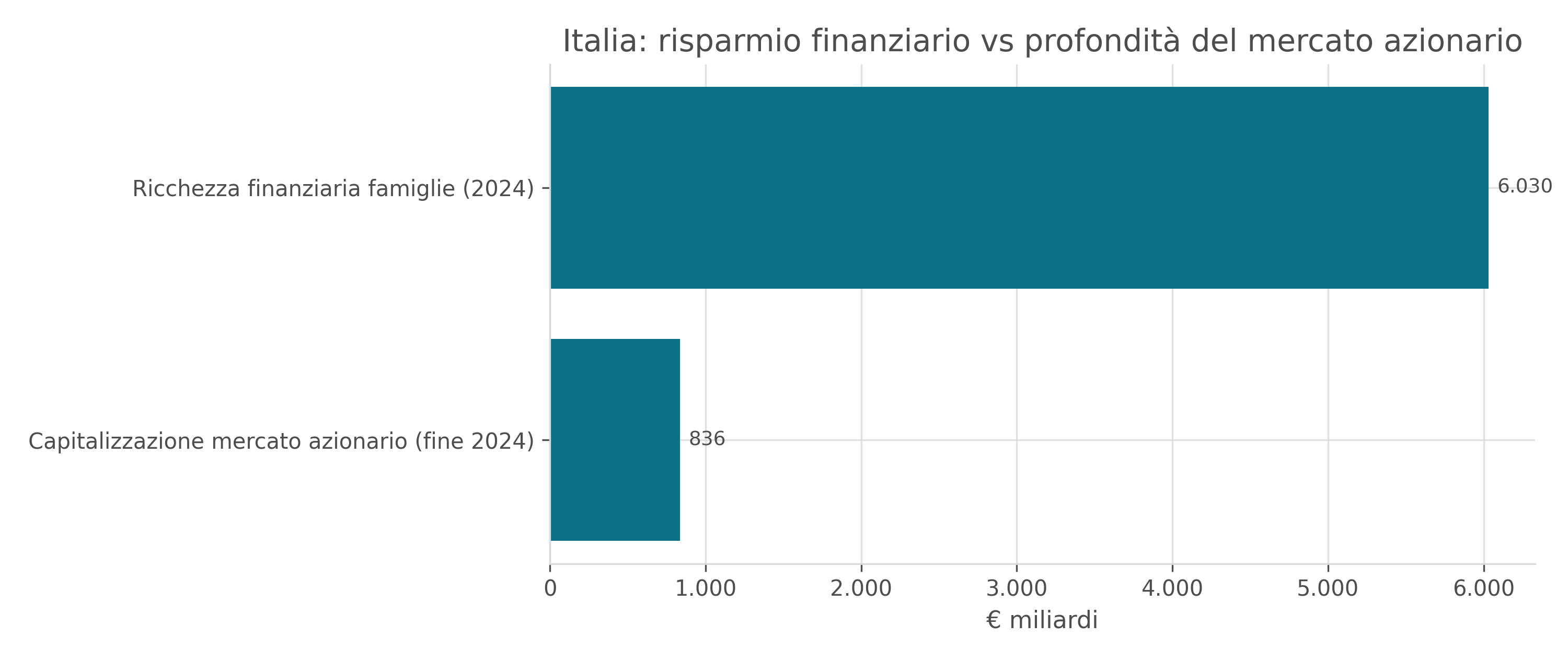

In the meantime, Italian families have exceeded 6,000 billion euros in financial wealth, with over 1,300 billion more accumulated since 2019. A significant portion is invested in products with a global underlying which they allocate mainly abroad, while Italian SMEs continue to live on self-financing and short-term bank debt, with very little equity to support succession, growth and supply chain M&A. The country is experiencing a paradox: the capital generated by the Italian real economy cannot find structured channels to return to the Italian real economy.

FIGURE 4 | Financial savings vs stock market depth

Source: Consob (market cap end 2024); FABI (financial wealth 2024).

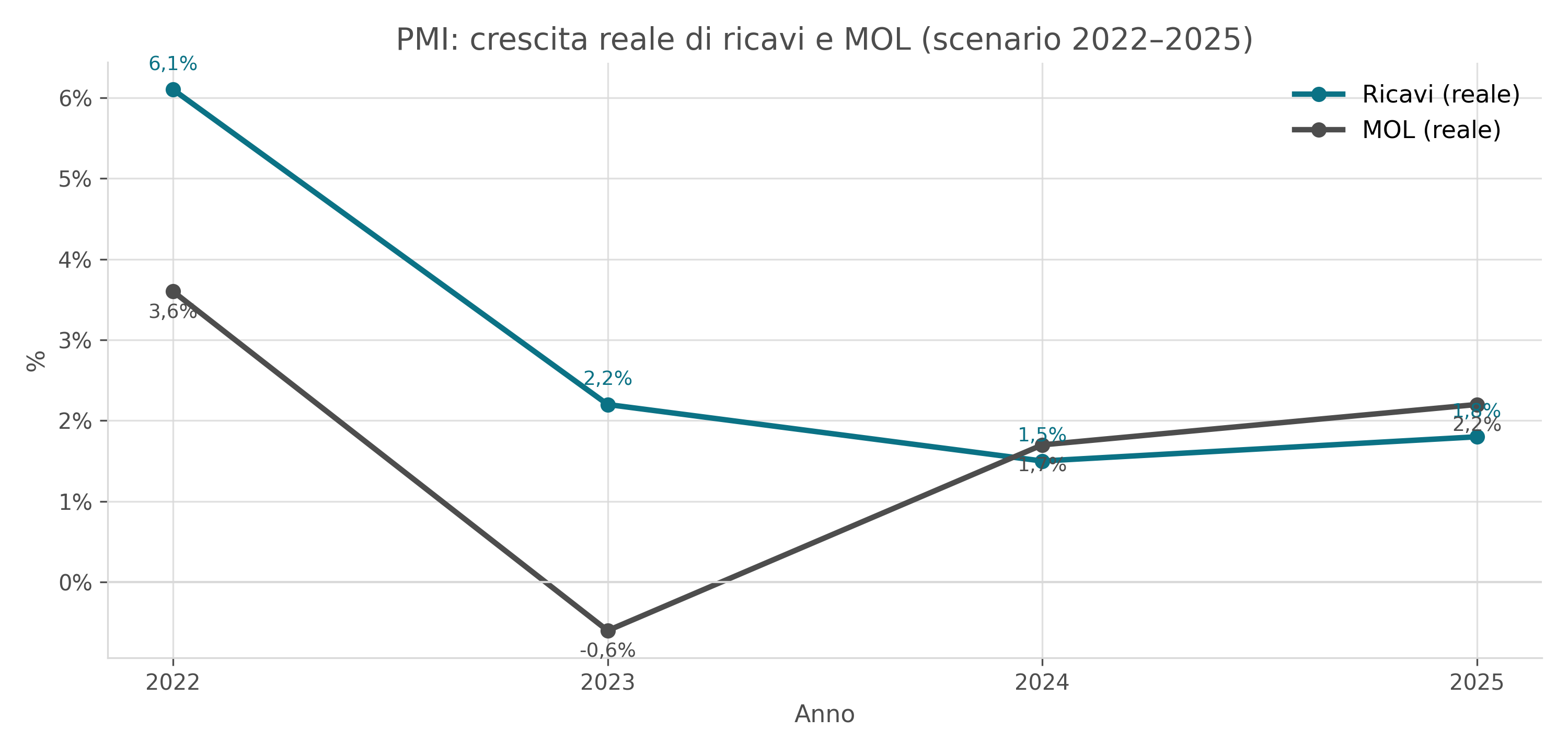

FIGURE 5 | PMI scenario: real growth in revenues and EBITDA (2022–2025)

Source: Cerved PMI 2023 (scenarios).

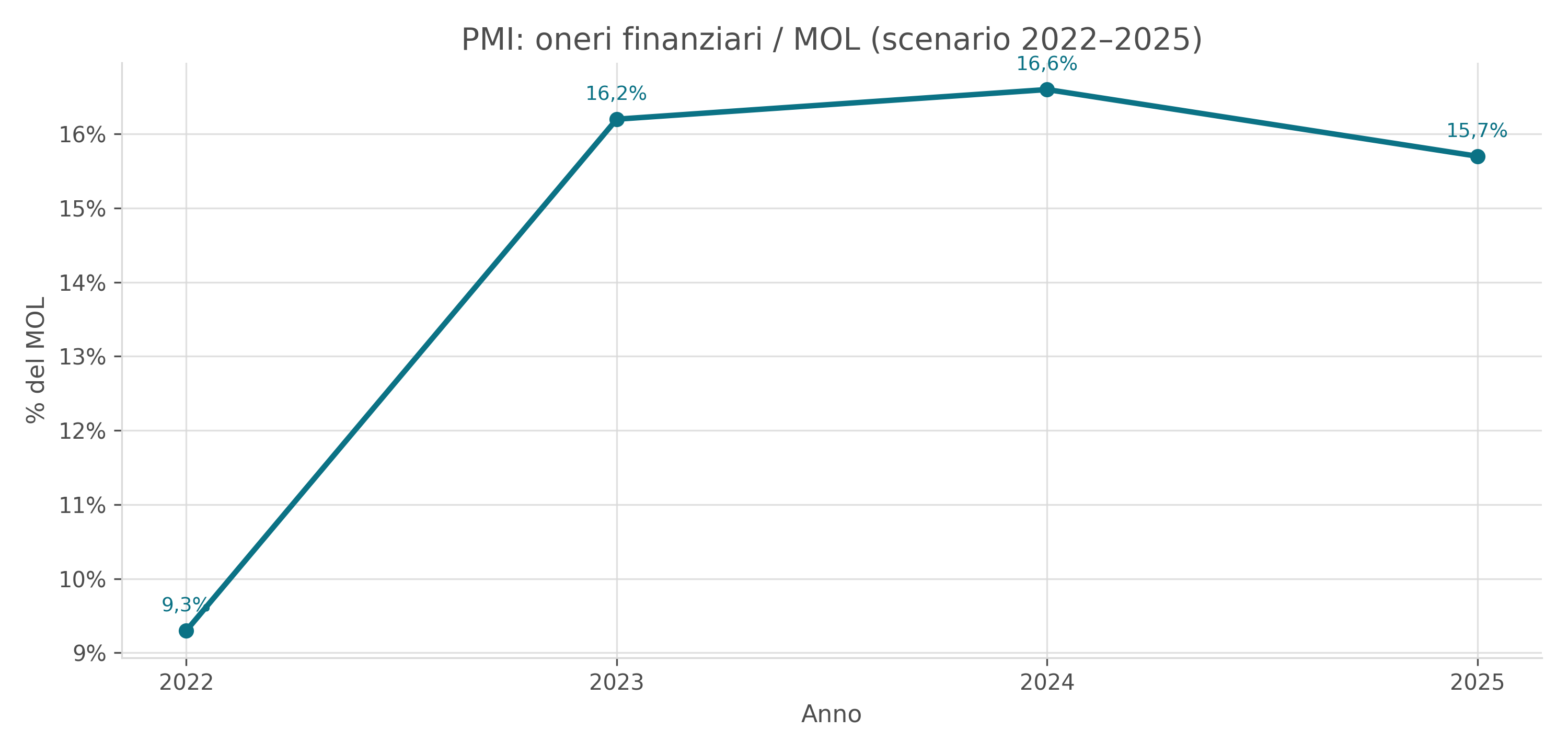

FIGURE 6 | SME scenario: financial charges/GOM (2022–2025)

Source: Cerved PMI 2023 (scenarios).

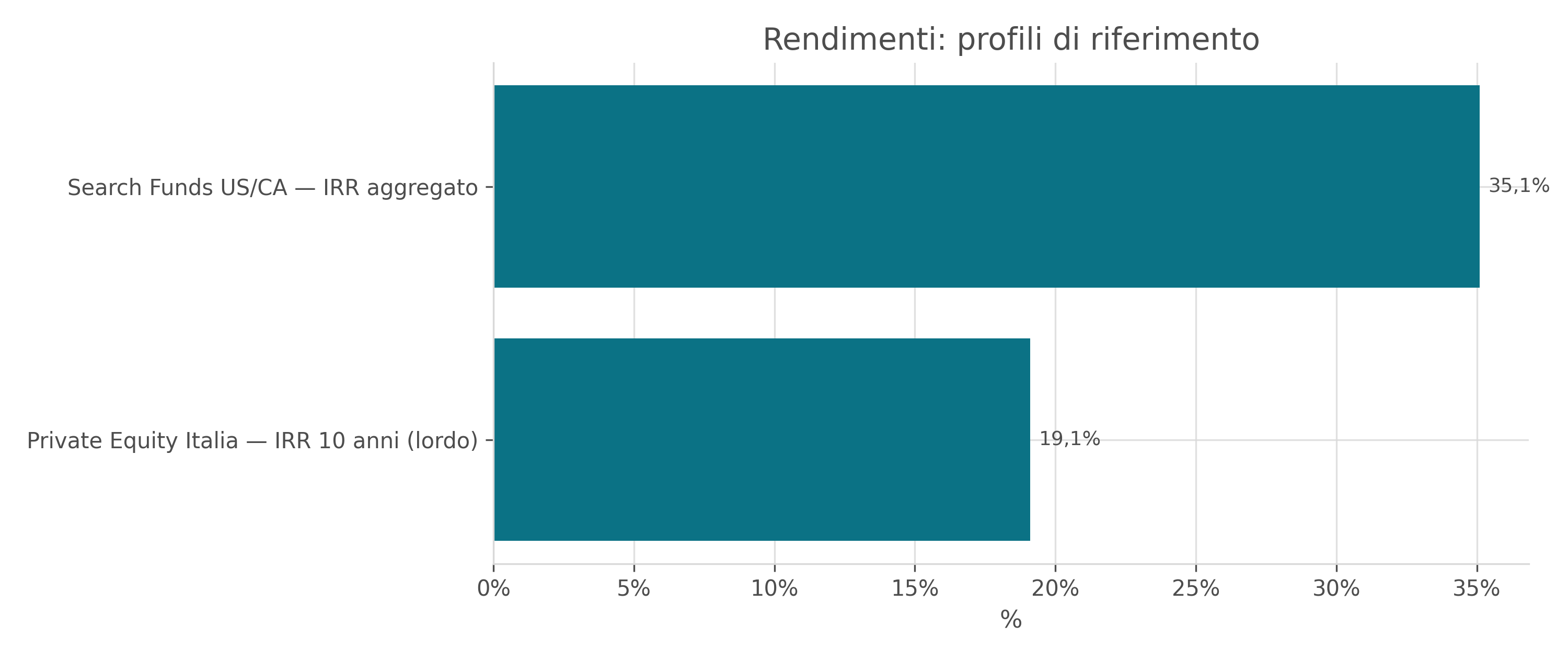

In this scenario, private capital itself is not the problem: KPMG–AIFI data indicates an average IRR of around 18–20% over the last ten years. The asset class, on paper, is capable of generating high returns and attracting part of the long-term savings. But the question is not whether private capital “works”: it is how it is built. If the return arises mainly from multiple expansion and deleverage, and little from industrial improvement, the solidity of that IRR is much less robust. A structural imbalance on deleverage means using cash flow for financial cosmetics - repaying debt and "raising" the multiple - instead of for plants, technology, people, R&D, i.e. for industrial competitiveness that creates real wealth for the system.

FIGURE 7 | Rendimenti: profili di riferimento

Source: KPMG–AIFI (IRR PE Italy); Stanford GSB (Search Fund Study).

Read from an industrial perspective, the numbers say otherwise: it is the right combination of capital and management, with an industrial perspective, that generates high and sustainable returns. But the majority of Italian companies are small or very small, therefore simply outside the radar of large asset managers, focused on a few national champions and, above all, on foreign large caps. For our SMEs, fundraising in equity is not a matter of choosing between many options, it is a structurally difficult effort. The real question is not whether private capital works, but how to design a private capital model that truly puts the country's industrial transition at the center.

The dividing line passes through the presence, or otherwise, of an industrial perspective and an operational managerial component in the capital value chain. It is one thing to build IRRs of 18–20% by compressing costs, pushing on leverage and selling to foreign funds or corporates. Another is to generate the same IRRs by structurally raising margins, productivity, ROIC, quality of revenues and supply chain resilience, maintaining governance and decision-making centers in Italy.

This is where the issue of patient capital and investment structure comes into play. For an SME that has to deal with generational transition, internationalization, process digitalization and one or two supply chain add-ons, 3–4 years are not enough: time periods of 7–10 years are needed. Capital must be coherent: not designed just to maximize a quick exit, but to accompany real industrial transformation. In this context, minority investment with well-defined board rights is a key lever. It is not a question of stopping at 30% out of timidity, but of building a balance in which the family remains the main shareholder - as well as, often, entrepreneurial guide -, private capital enters with a significant but not totalitarian share, sits permanently on the board, has a say on the industrial plan, supply chain M&A and capital allocation. The goal is not to replace the entrepreneur, but to put the company in a position to survive and grow beyond its generation.

A further element, often underestimated, is engagement with the entrepreneur. In most cases we are talking about extraordinary figures in terms of the product and the commercial relationship in their "natural zone", but also instinctively distrustful and individualistic. Without demanding panaceas or asking for acts of faith, experience shows that the ability to build a bridge of trust between finance, managerialization and entrepreneurship is the most decisive step. A minority entry that does not want to replace the entrepreneur, but rather build a shared industrial perspective with him, is not a negotiating detail: it is a necessary condition for the structural growth of our real economy, especially manufacturing.

As a manager who works at the intersection of technology, finance and industry, I come to a simple belief: finance alone is not enough, but entrepreneurship alone is not enough either. We need a balanced triangle between entrepreneur, capital and management. The entrepreneur brings history, risk and the ability to decide in incomplete conditions; capital brings horizon and discipline; management reads markets, technologies, competition, regulation and translates capital into operational choices. The point is not to put the Operating Partner at the center, but to truly integrate the industrial perspective into the capital decision chain.

It is from this perspective that Askéon Capital was born. Askéon presents itself as an industrial partner of companies considered "micro" (between 3 and 30 million in turnover) but with enormous industrial and strategic potential, not as a flipping vehicle. It works with entrepreneurs, not against them, keeping families as key shareholders and placing third-party capital in an active minority position, with clear delegations to accompany the industrial plan, governance and M&A of the supply chain. The creation of value is not entrusted to multiple expansions, but to four concrete levers: structural improvement of margins, quality and diversification of revenues, efficiency of invested capital, financial and supply chain resilience.

In a country where SMEs represent 99% of businesses and generate a large part of the added value and employment, this is not a niche strategy: it is, essentially, industrial policy made with private instruments. In the next five to ten years, Italy will play a decisive part in its industrial future. We can continue with episodic interventions, letting capital enter and exit according to global logic, or consciously decide to become a country of organized private markets, where Italian savings finance, with adequate returns, the companies that truly make the country.

In the end, the difference between an operation that generates IRR by slowly emptying a piece of Italy and an operation that produces the same IRR by strengthening its industrial backbone is not made by the slogans, but by the architecture: financial, industrial and managerial integrated into the decisions. Everything else - green, digital, ESG, AI - is instrumental: very powerful if inserted into this logic, perfectly useless if it remains a slogan hanging from a system that continues to crumble, one succession after another. The time to choose is not "when rates will fall" or "when the stock market will restart". The time is now.